This reflects how we would best position a portfolio of fixed-income ETFs to achieve maximum total return over a comparable baseline neutral portfolio of fixed-income securities (benchmark).

Duration – Relative Allocation: 90% of Benchmark

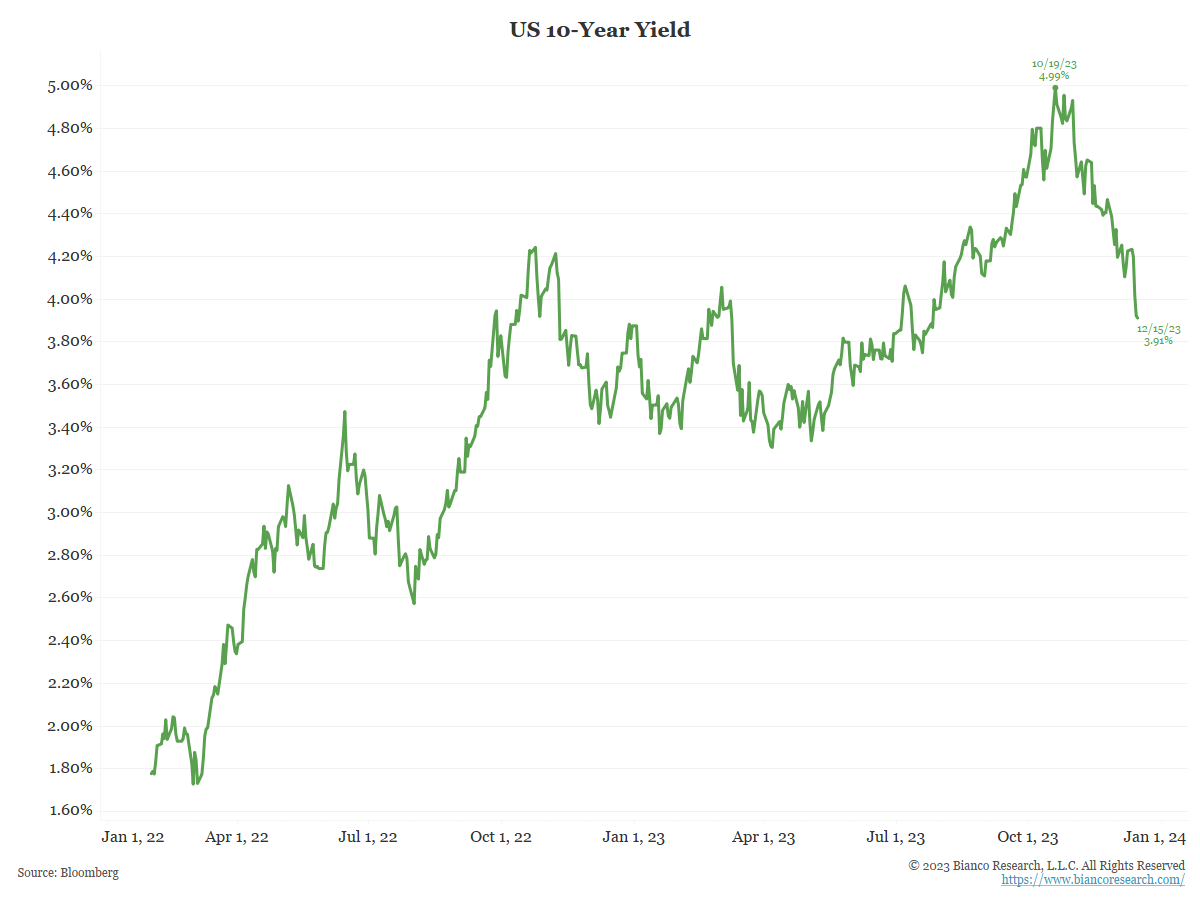

The index is underweight duration, based on the belief rates could head higher.

The chart shows the 10-year yield was recently at a 16-year high. While yields have fallen since October, we do not believe this trend is over.

Curve: Neutral

The current position is to mimic the curve weightings of the broad-based fixed-income index. In other words, there is no “tilt” in our positioning.

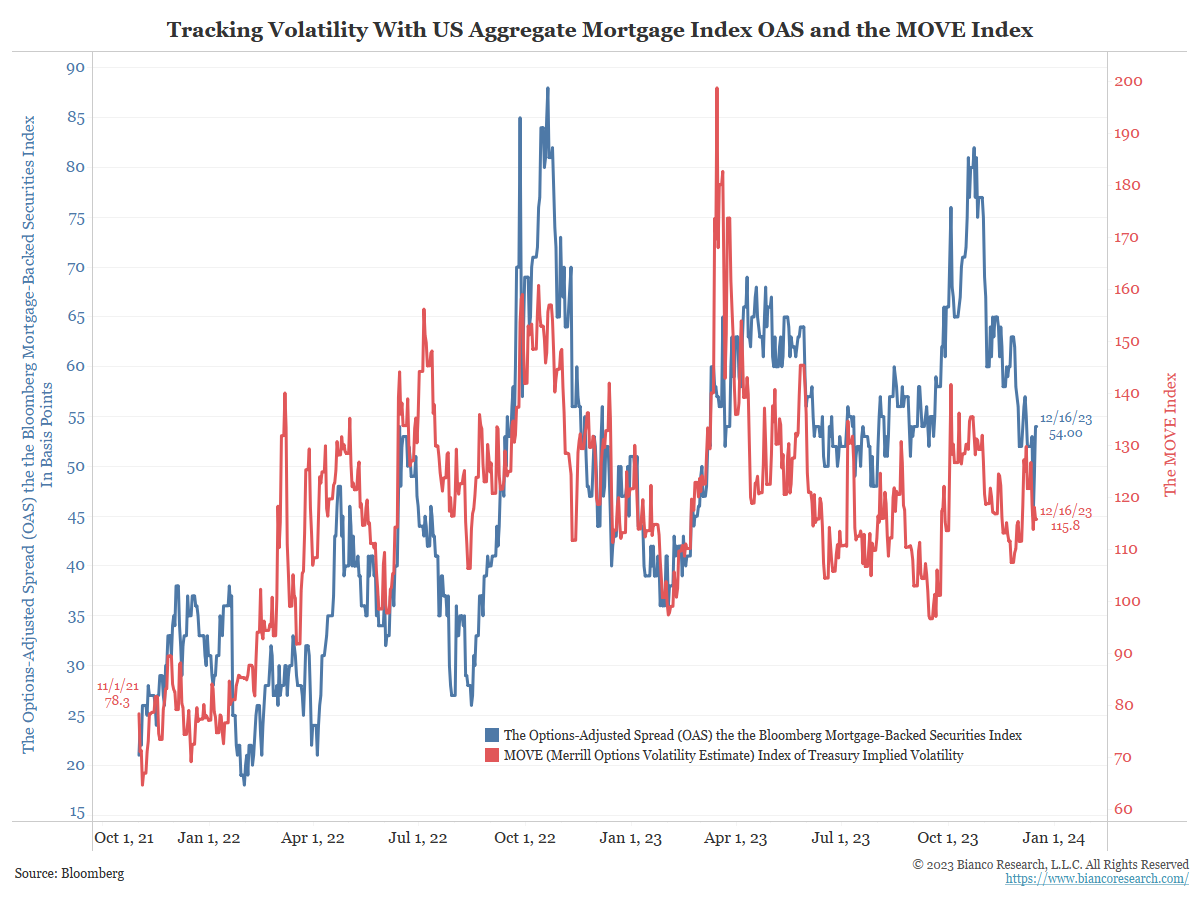

Structure / Securitized – Sector Allocation: 71% of Benchmark

The characteristics table shows the tilted index holds 71% of the securitized (mortgages) product compared to the benchmark.

All mortgages have an embedded option because holders can pre-pay their mortgage anytime. Because of this structure, the option-adjusted spread (OAS) of mortgages (blue line below) and the MOVE Index (red line), which measures the implied volatility of 30-day interest rate options, have a tight relationship.

Given the uncertainty surrounding inflation, Fed policy, and the belief that rates will move higher, look for interest rate volatility to move higher, causing mortgage OAS to widen.

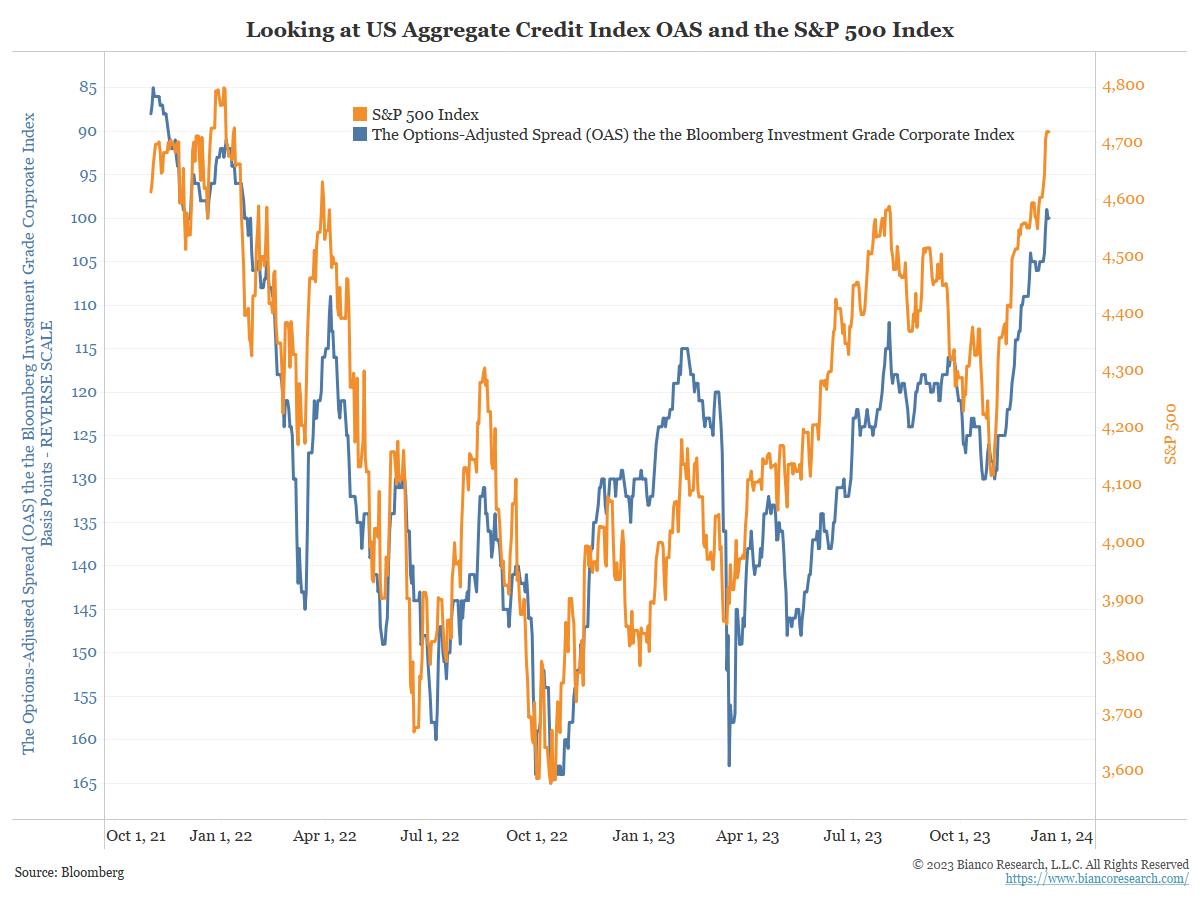

Credit – Sector Allocation: Neutral

The index holds 98% of the corporates in the benchmark. In other words, the tilted index holds an effective neutral credit allocation and remains neutral by quality.

The chart shows investment-grade corporate spreads (blue) and the S&P 500 (orange) move in tandem. Relative credit performance moves with equity prices.

Outlier – 20% of the Portfolio in 0-5 Year TIPS

The index holds a 20% allocation to 0-5 year TIPS as inflation protection. This is “outside” of the benchmark.

The index has a bias for owning short-maturity inflation securities (TIPS). The 2-year inflation break-even rate is ~220bps. The committee anticipates inflation to exceed 2.20% over the next two years. Short-maturity inflation protection is attractive, especially if inflation remains sticky and persistent.