By Jim Bianco

2024 Performance Review

2024 completed our first calendar year managing The Bianco Research Total Return Fixed-Income Index. You can find more about it here or on Bloomberg at BTRINDX <Index>.

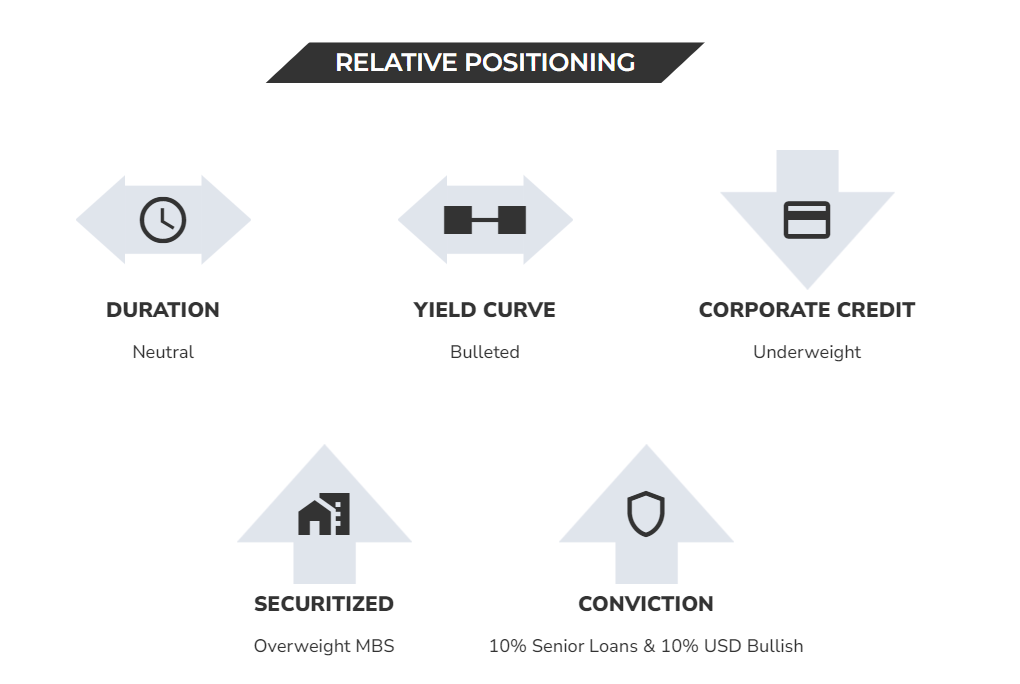

A reminder: we discretionarily manage our index, or “tilt,” by over- or under-weighting various characteristics. Our latest tilts are below and the rationale can be found here.

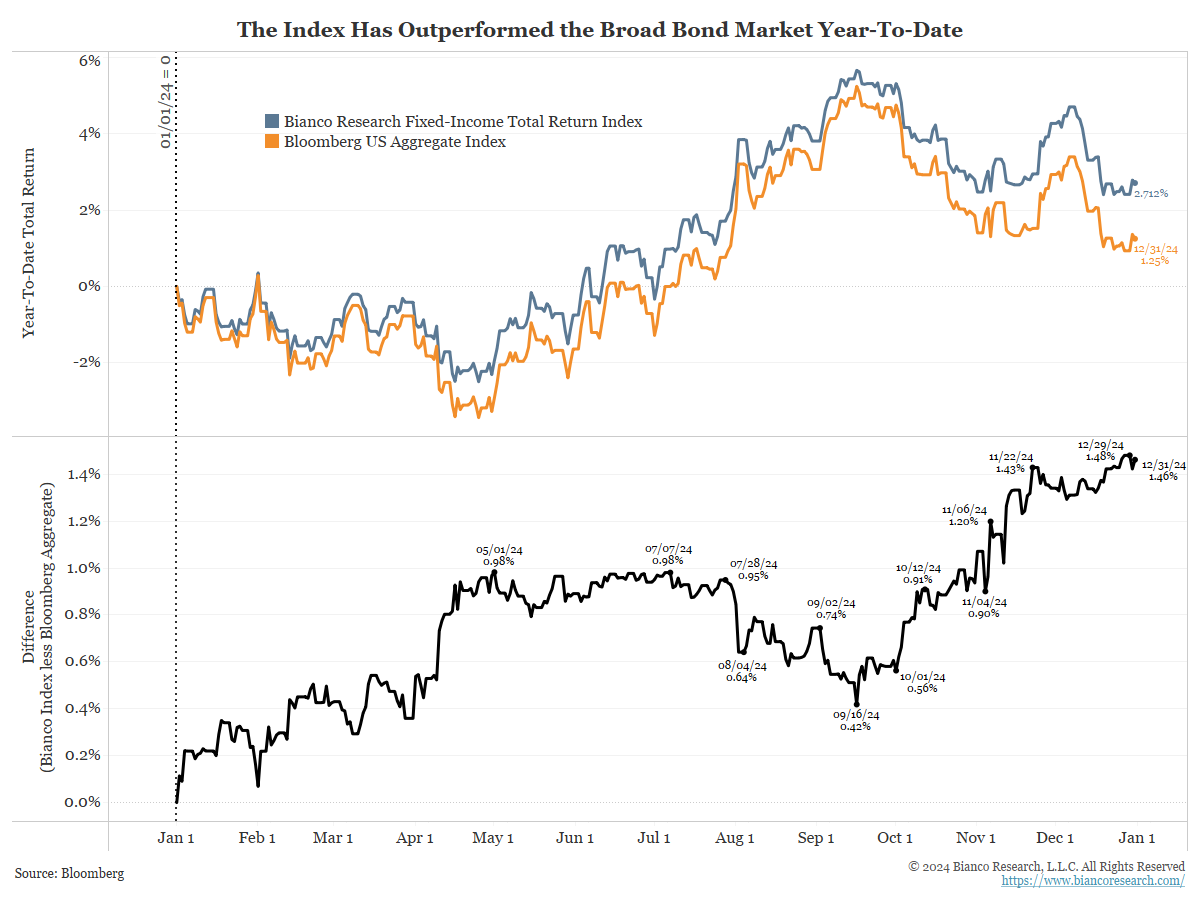

As the following chart shows, our index (blue) outperformed a broad investment-grade benchmark (the Bloomberg US Aggregate Index, orange) by 146 basis points (black) in 2024.

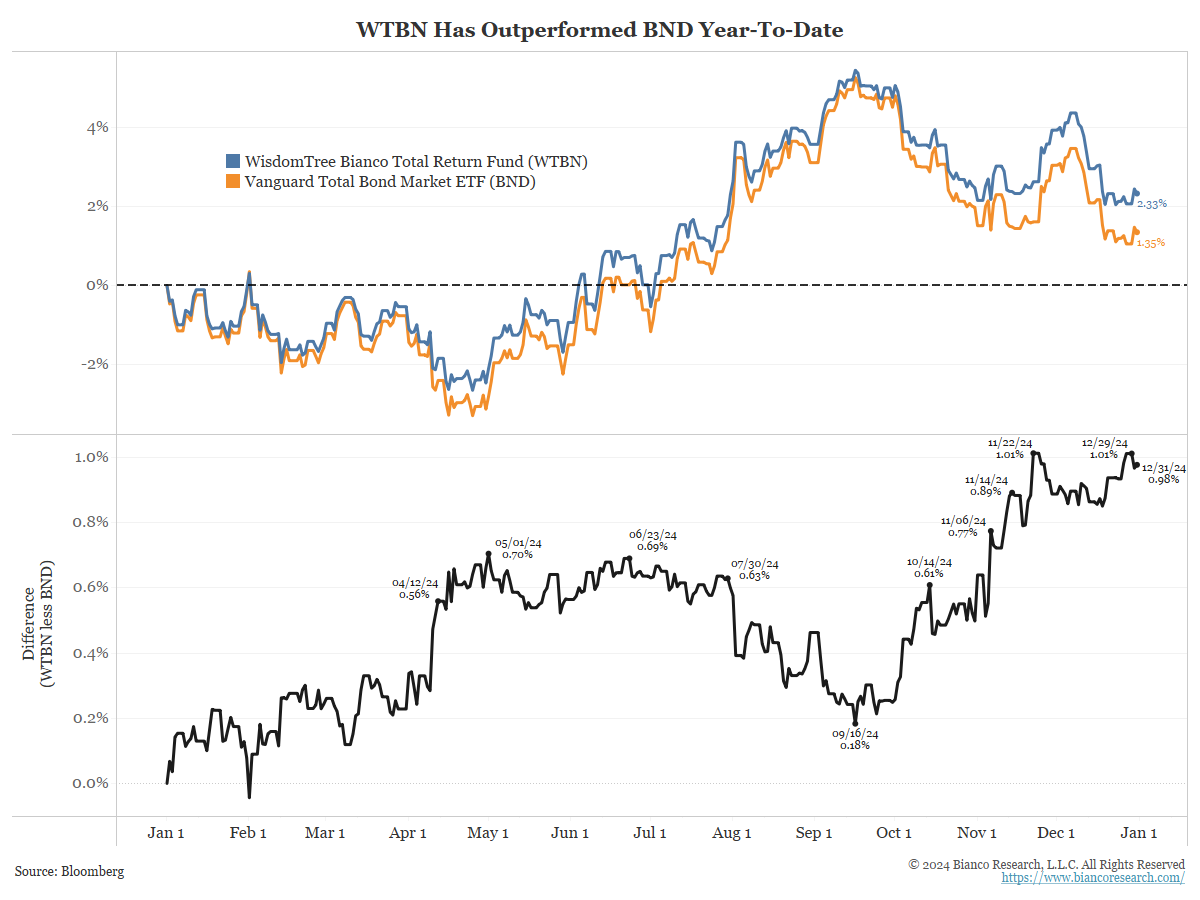

The WisdomTree Bianco Fund (WTBN) tracks our index, similar to how the Vanguard Total Bond Market ETF (BND) tracks the Bloomberg US Aggregate Index.

As the next chart shows, WTBN (blue) outperformed BND (orange) by 98 basis points (black) in 2024.

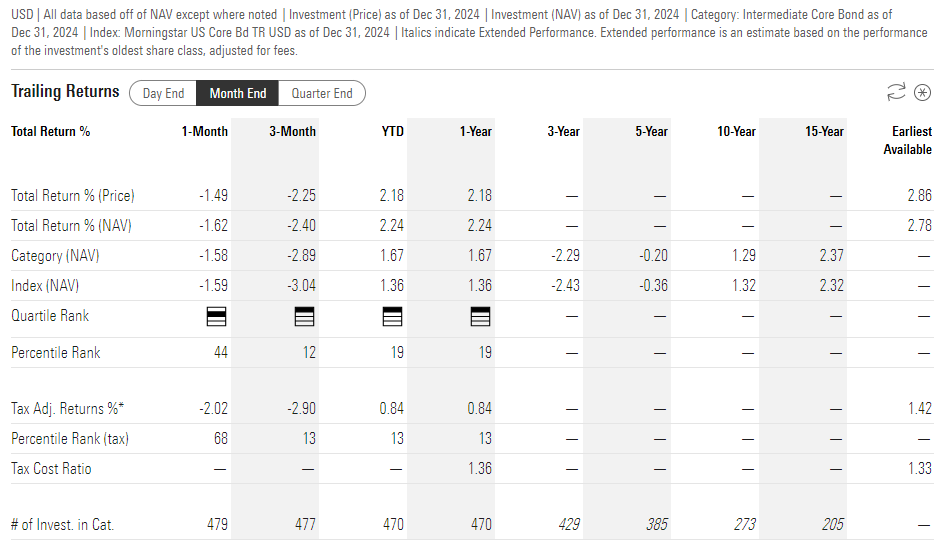

On a relative basis, Morningstar places WTBN in the core bond category along with 470 other funds. In 2024, WTBN ranked in the 19th percentile, meaning it outperformed 81% of this universe. Its tax-adjusted return was in the 13th percentile (meaning it outperformed 87% of the universe).

Finally, the American Association of Individual Investors (AAII) grades ETFs. At the end of 2024, WTBN received an “A.”

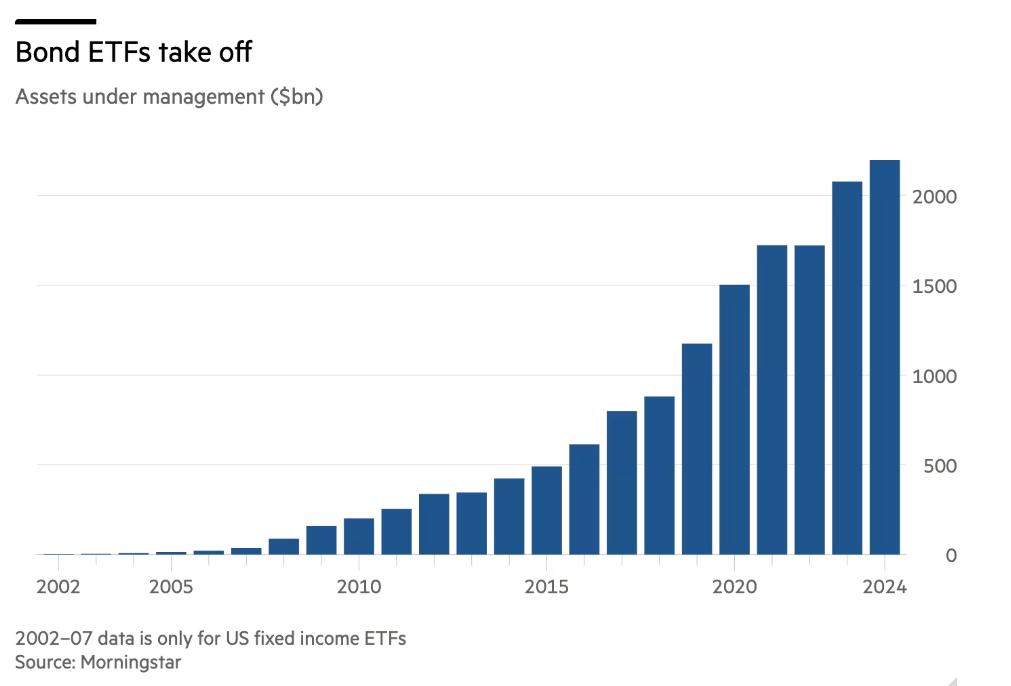

ETFs Are Eating the World

Our index is somewhat unique in the world of fixed income. We construct our index using other fixed-income ETFs, which keeps the tracking error of our broad-based benchmark low compared to other index-tracking funds. You can find WTBN’s ETF holdings here.

In July, The Financial Times penned the following 6,000 word piece.

- The Financial Times – (July 30. 2024) Robin Wigglesworth and Will Schmitt: ETFs are eating the bond market

And changing its nature in the process

Some ETF believers were sceptical that the vehicles would ever prove successful in fixed income. They were wrong. This is no longer a niche. In fact, fixed income ETFs — now a $2tn asset class — are shaking up the old order in a shadowy but important pillar of finance that has long been ruled by big banks and investment groups. Even the assets under management chart above understates how powerful this trend is. After all, the past few years have not been kind to the bond market, depressing the value of most fixed-income ETFs and obscuring huge inflows. Even in 2022 — one of the worst years in history for the asset class — bond ETFs attracted $245bn of investor money. They have taken in another $195bn so far this year.

I’ve been in the bond market for over 35 years, and frankly, I now question the need for a manager to use fixed-income securities to construct a fixed-income portfolio. A fixed-income ETF is faster, cheaper, more transparent, and more liquid. And with hundreds of fixed-income ETF offerings of every strip and flavor and seemingly more coming daily, why wouldn’t you construct a portfolio using fixed-income ETFs instead of owning thousands of illiquid and hard-to-value securities?

BND holds 18,071 securities as of December 31. We have structured our index with just nine fixed-income ETFs at year-end (we used as many as 14 earlier this year). Coincidentally, the sum of these nine ETFs holds 18,072 unique securities, one more than BND. However, our index has different weightings and holds many securities not included in BND. Fixed-income ETFs allow replicating a broad diversified portfolio without the complexities and costs of owning thousands of bonds.

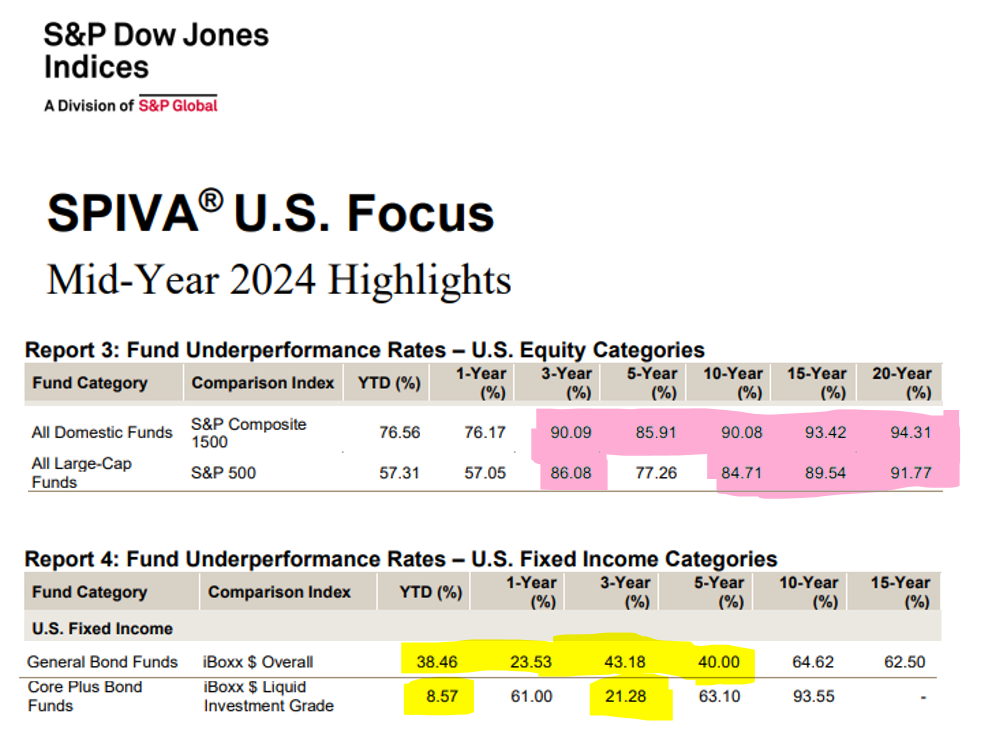

Actively Managed Bond Funds Work!

Some may doubt actively managed funds’ ability to beat a benchmark. Almost no equity funds can beat the benchmark like the S&P 500, but fixed income funds are different.

S&P publishes its “Index versus Active” report, known as SPIVA, twice yearly. The latest is for mid-year 2024. This report details active managers’ performance relative to their benchmark. We pulled SPIVA tables from the latest report, highlighting the broad stock and bond categories.

These tables highlight the percentage of funds that underperform their benchmark. The areas highlighted in pink indicate horizons in which more than 80% of funds underperform. The areas highlighted in yellow show horizons in which less than 50% underperformed (or, the majority outperformed). Most equity managers cannot beat their benchmark, but many fixed-income managers can.

In a May op-ed we wrote for The Financial Times, we offered reasons why active fixed-income managers can beat a benchmark while equity managers find it much harder.

- The Financial Times (May 9. 2024) – Jim Bianco: The total return strategy in bonds is far from dead

The end of the historic bull market in the asset class just means a different approach is needed from investors

In equities, your biggest weightings are the all-stars. Think of the Magnificent Seven stocks. Equity managers cannot beat an index fund if they are not always all-in on the all-stars, and most are not. However, in the bond market, the biggest weightings are often the problem children, such as overleveraged companies, low-coupon mortgage securities, and countries that borrow too much debt. Recognising problems and sidestepping them produces big rewards. The fact that most managers have beaten a benchmark index confirms this. The new era just needs a change of style with more focus on coupon protection and risk assessment.

Investing Is More Than Momentum

So far, we have shown our index performed much better than the Bloomberg US Aggregate, leading to WTBN being a top-quartile performer in Morningstar’s Core Bond category. We also showed outperformance in actively managed bond funds is much more common than in actively managed equity funds.

Hopefully this sounds compelling, but we are left with one crucial problem: Our fixed-income index total return was 2.71% in 2024. This compares unfavorably to the 5.29% total return for the 3-month Treasury bill, 8.19% for high yield, 18.67% for the MSCI World-Free Index, 25.02% for the S&P 500, 26.62% for gold, and 120.5% for bitcoin.

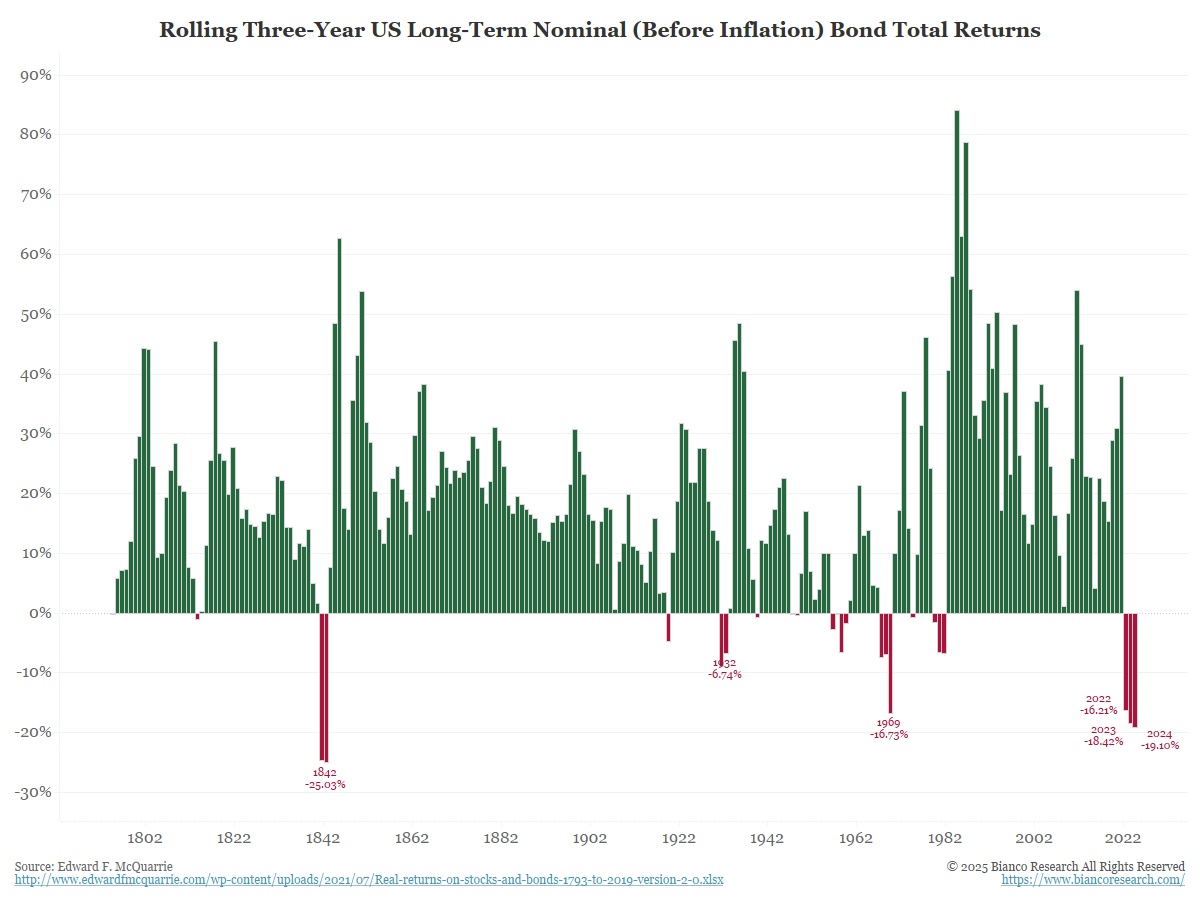

In addition, as the following chart shows, the last three years have been the worst stretch for bonds in 180 years (no typo)!

When central banks manipulate interest rates to zero (or negative, as in Europe and Japan), getting off these low rates means a lot of pain for investors. This is due to the properties of positive convexity causing long durations at low yields and the lack of cushion from coupon income.

The good news is that the pain of correcting this manipulation is essentially behind us. With yields up a lot, leading to shorter durations and much larger coupon income, the pain from potentially higher rates in the future would be nothing like the last three years. See 2024, which was not a good year, yet broad fixed-income indices finished with positive returns.

Momentum is but one factor in investing. Another factor that might be more telling about future returns is valuation.

Valuations Always Matter

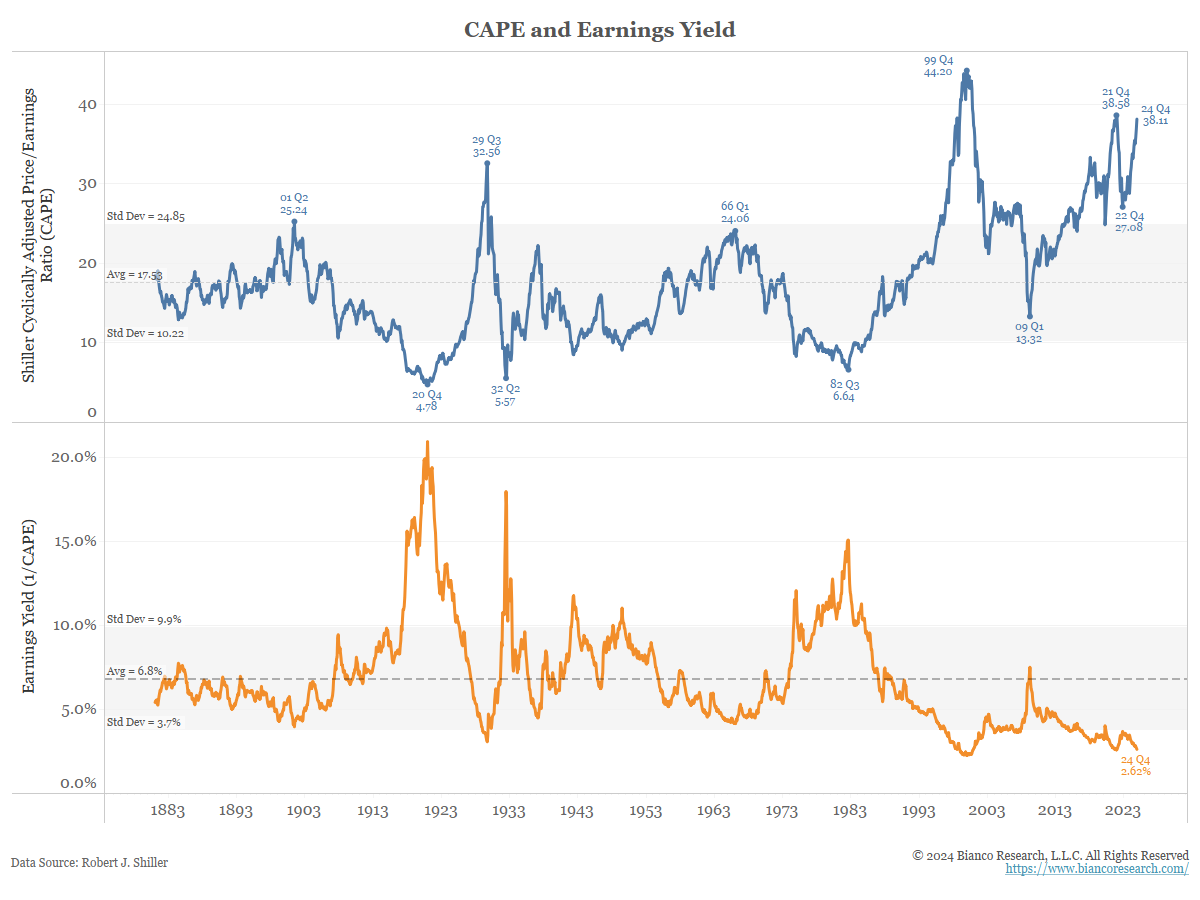

Yale Professor Robert Shiller won the 2013 Nobel Prize in Economics for his work on valuing asset prices. He found the concept simple: the higher the valuation, the lower the expected (or future) return.

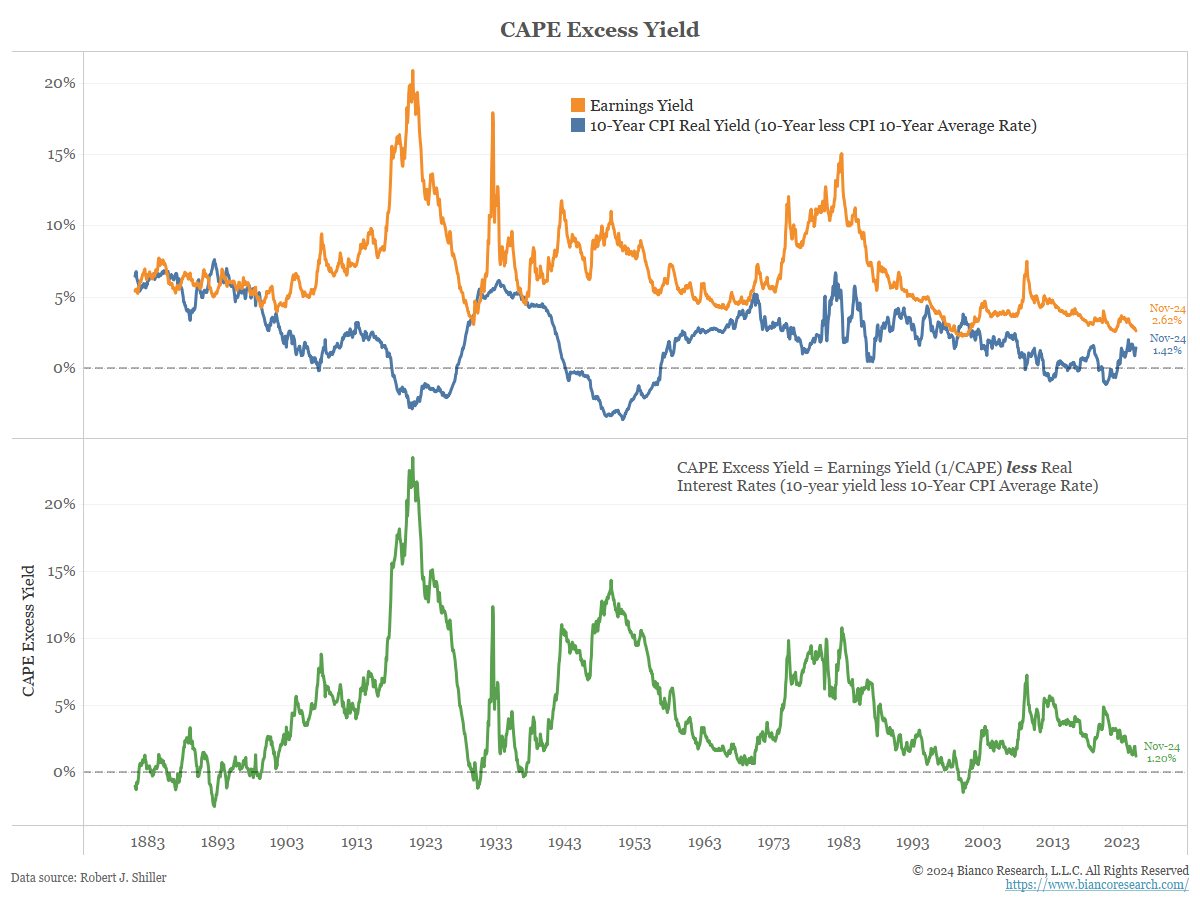

Shiller is famous for his Cyclically Adjusted Price/Earnings Ratio, or CAPE. It is shown below in blue. The bottom panel (orange) shows the earnings yield, which is the reciprocal of CAPE.

The next chart compares the earnings yield from above (orange) to real 10-year yields (blue).

The bottom panel above (green) shows the CAPE excess yield (orange less blue). This measure is the premium an investor should expect above a long-term real (inflation-adjusted) yield over the next decade. Currently, it is just 1.2%.

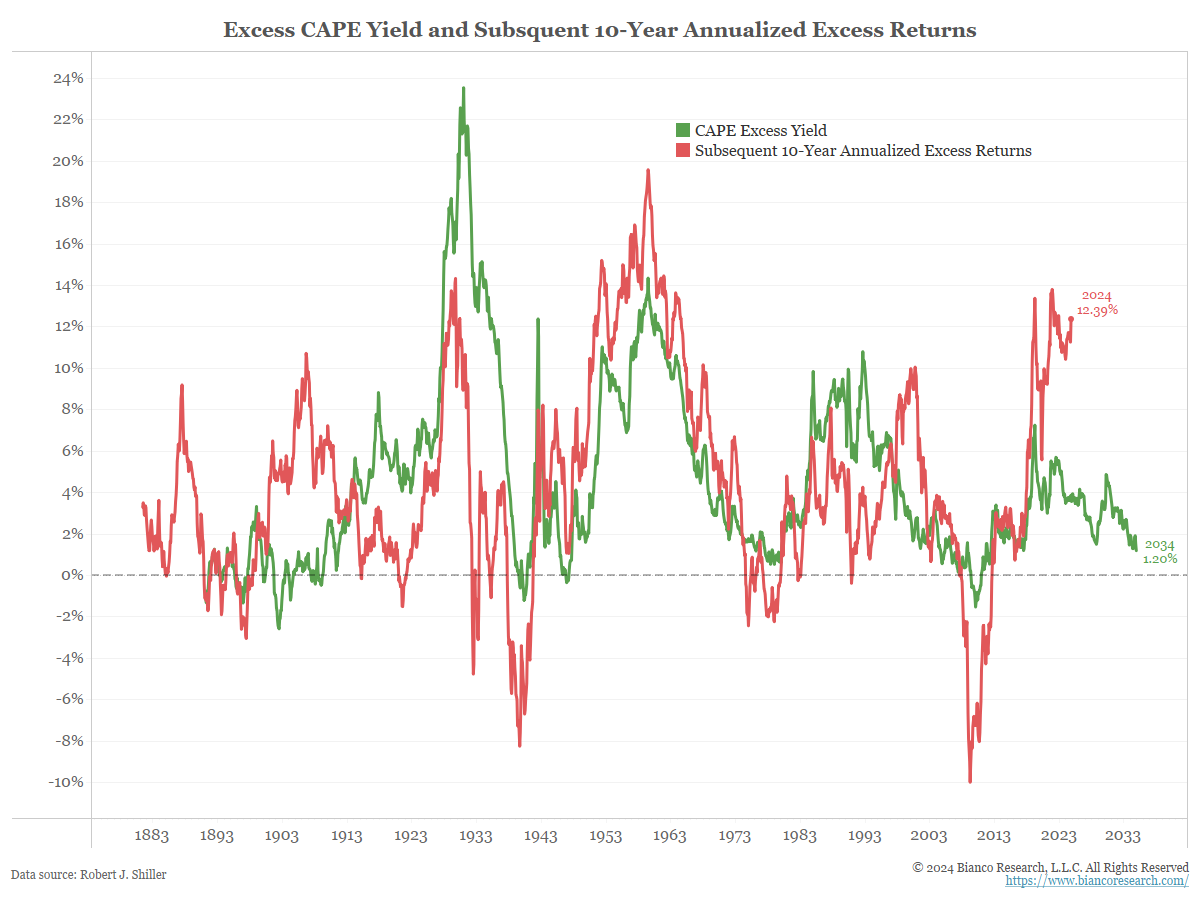

The final chart in this series shows the CAPE excess yield from above shifted forward 10 years (green, out to 2034) as a sign of what is expected over the next decade. It is overlaid with the actual excess (above real yields) returns (red) to show how good a guide CAPE excess returns have been. Not bad.

Cliff Asness of AQR made this same point in his 2025 investor letter, reviewing the previous 10 years from the perspective of 2035.

- AQR – Cliff Asness: 2035: An Allocator Looks Back Over the Last 10 Years

First, it turns out that investing in U.S. equities at a CAPE in the high 30s yet again turned out to be a disappointing exercise. Today the CAPE is down to around 20 (still above long-term average). The valuation adjustment from the high 30s to 20 means that despite continued strong earnings growth, U.S. equities only beat cash by a couple of percent per annum over the whole decade, well less than we expected.

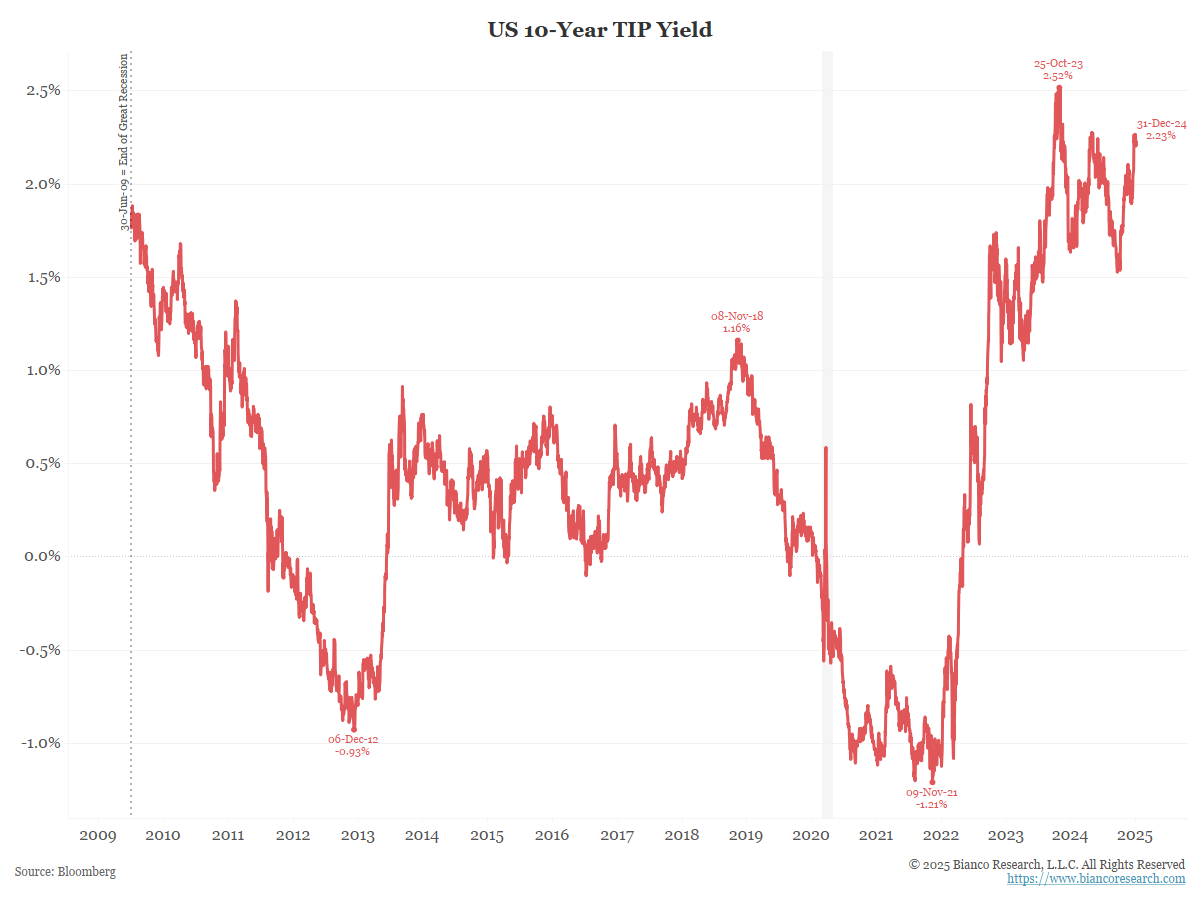

From a nominal perspective, the 10-year Treasury Inflation-Protected Security (TIPS) is an excellent proxy for the market’s estimate of real yields over the next decade.

The next chart shows the marketplace expects a 10-year real yield of 2.23%.

So, assuming a 3% inflation rate over the next decade, the 10-year yield should average 5.23% (3% inflation plus 2.23% real yield), and stocks should average a return of 6.43% (5.23% 10-year plus the CAPE excess yield of 1.2%).

These expected returns mean fixed income should be competitive with stocks. The era of TINA (there is no alternative) is over. What does this mean for portfolio construction?

Bonds Are No Longer Crash Insurance

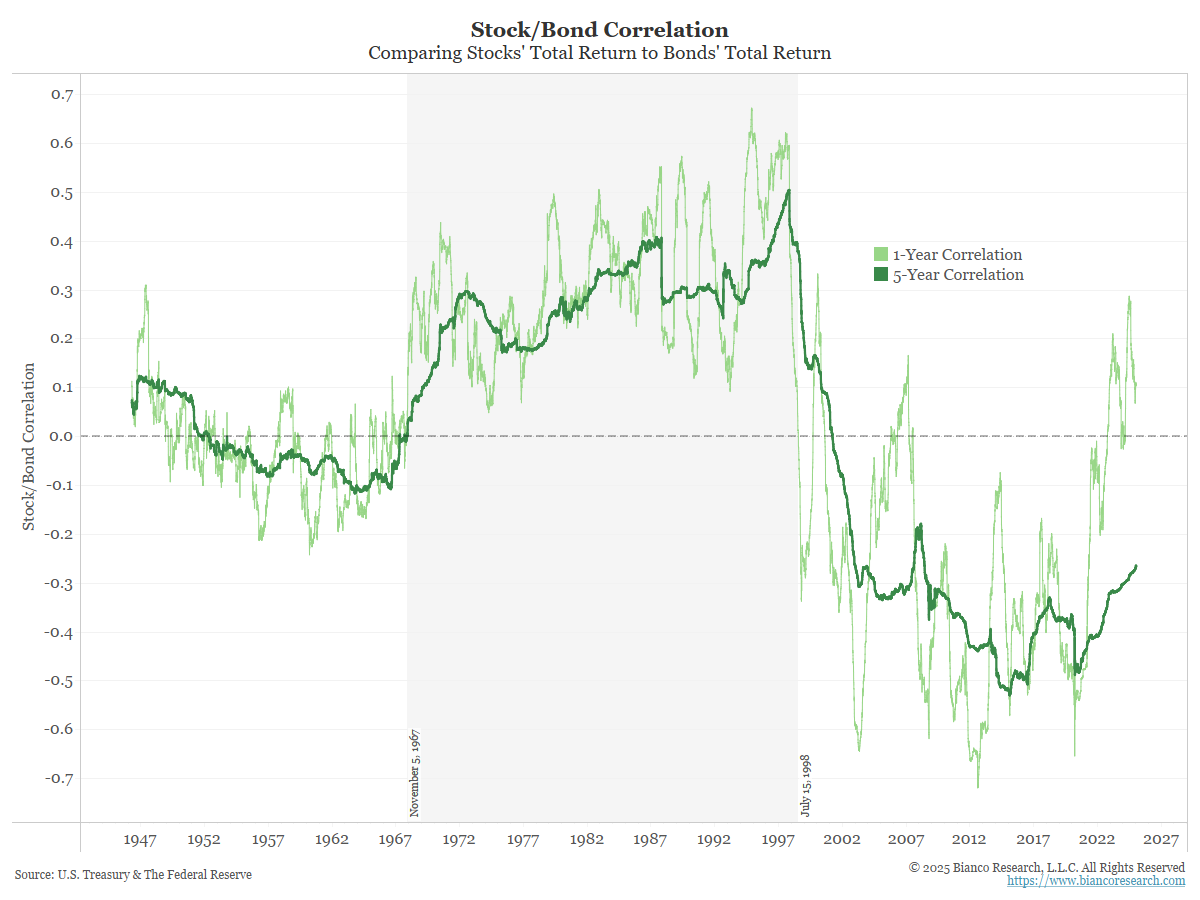

The modern 60/40 portfolio concept is built around the idea that stock and bond total returns should move in opposite directions (negatively correlated) and act as a hedge against one another or crash insurance for stocks. This was true for most of the period between 1998 and September 2022. The chart below shows that the correlation between stock and bond total returns was negative during most of this period.

After September 2022, however, the 1-year correlation between stock and bond returns turned positive (light green line). In other words, once the correlation turned positive, bonds were not a hedge for stocks. Why might this have changed? We have often argued the market’s view of inflation has governed the relationship between stocks and bonds.

The shaded area in the chart above highlights the period from 1967 to 1998 when the correlation between stock and bond returns was positive. During this period, high inflation concerns drove this relationship. When markets were relieved, there was no inflation, bond yields went down (prices went up), and stock prices went up. When the markets worried inflation was heating up, bond yields went up (prices went down), and stock prices went down.

When the rolling correlation was largely negative from 1959 to 1967 and 1998 until September 2022, the main concern was a deflationary mindset. Bond and stock prices moved opposite of each other. Why? When the market worried about deflation taking hold, yields fell (prices rose) alongside falling stock prices. When the market was relieved that there was no deflation, yields rose (prices fell) while stock prices rose. From this environment, the modern 60/40 portfolio construction was born.

In the last few years, stock and bond prices behaved like they did from the 1960s to the 1990s. They move up and down together, negating one of the key reasons for creating a 60/40 portfolio. Bonds are no longer crash insurance. This doesn’t mean the 60/40 portfolio is dead. It simply means the reason for holding bonds is changing.

Instead, bonds are now a low-volatility, competitive alternative to a broad holding of stocks. While the reason for holding bonds may be changing, the same 40% weighting in a portfolio makes sense. With stock valuations high and expected future returns low, why not keep a core holding in a low-volatility asset like bonds that might offer a similar return over a long horizon?

Below is our idealized portfolio:

- 40% actively-managed fixed income, looking for 5.25% annualized returns over the next decade

- 20% a passive basket of stocks, such as the S&P 500, looking for 6.4% annualized returns over the next decade

- 30% “hot sauce” (credit Eric Balchunas of Bloomberg for the term). This concept has high expected returns that come with high risk. Examples are alternatives, growth stocks, AI, crypto, etc. Target 9% to 10% annualized returns as a group

- 10% cash until the yield curve gets very steep (say the 10-year to 3-month spread above 150 basis points), then collapse this into fixed-income. Currently, this could produce a 4.25% to 4.50% annualized return

We look forward to our second year, learning more things while working to make it as successful as the first year.